Whole Life Insurance Investment – Embarking on the journey of wealth accumulation and long-term financial security often involves exploring various avenues, and for many, life insurance transcends its primary protective purpose to become a strategic financial tool. Whole life insurance, in particular, offers a unique proposition, blending a guaranteed death benefit with a cash value component that grows over time on a tax-deferred basis. This dual nature positions it not just as a safety net for loved ones, but as a potential asset within a diversified financial portfolio. Understanding its intricacies is key to leveraging its full potential.

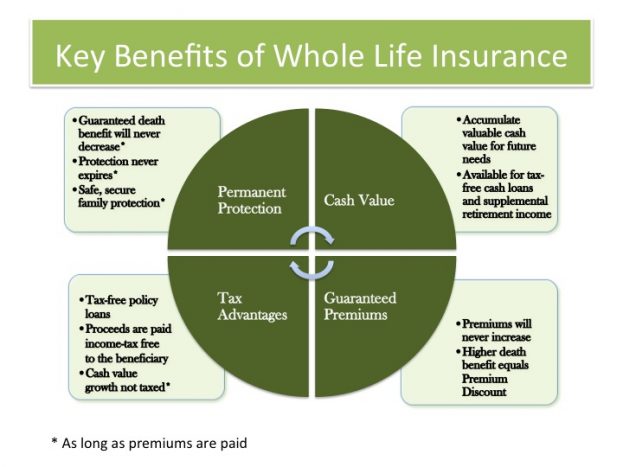

At its core, whole life insurance provides lifelong coverage, meaning the policy remains in effect as long as premiums are paid. Unlike term life insurance, which covers a specific period, whole life offers permanence. Crucially, a portion of each premium payment contributes to the policy’s cash value, which grows at a guaranteed rate. This growth is often supplemented by dividends from the insurance company, further enhancing its accumulation potential. This steadily increasing cash value can be accessed during the policyholder’s lifetime, offering a flexible financial resource for various needs, from supplementing retirement income to covering unexpected expenses.

The “investment” aspect of whole life insurance stems from this growing cash value. While it may not offer the rapid, high-risk returns of some other investment vehicles, its guaranteed growth, tax deferral, and the added security of a death benefit make it an attractive option for those seeking stability and predictable long-term gains. It’s a strategy that appeals to individuals who prioritize security, guaranteed growth, and the peace of mind that comes with a financial product designed for longevity. Exploring whole life insurance as an investment requires a nuanced understanding of its features, benefits, and how it can be strategically integrated into broader financial planning.

Whole Life Insurance Investment

Understanding Whole Life Insurance as an Investment Vehicle

Whole life insurance, often perceived primarily as a death benefit tool, possesses a sophisticated investment component that many overlook. This unique financial product blends permanent life insurance coverage with a cash value accumulation feature that grows on a tax-deferred basis. For individuals seeking a stable, long-term financial strategy, understanding the investment aspects of whole life insurance is crucial. It’s not a get-rich-quick scheme, but rather a deliberate approach to wealth building and preservation, offering a predictable growth trajectory alongside lifelong protection.

The core of whole life insurance investment lies in its guaranteed cash value. A portion of your premium payments is allocated to building this cash value, which grows at a guaranteed minimum interest rate set by the insurance company. Beyond this guaranteed growth, many policies also participate in the insurer’s profits through dividends, which can further enhance the cash value’s growth. Similarly, when managing your financial protection, you should compare the Best Car Insurance Companies USA. These dividends are not guaranteed but have historically provided a significant boost to the returns of many participating policies. This dual mechanism – guaranteed growth and potential dividends – makes whole life insurance a compelling option for those prioritizing security and steady accumulation over market volatility.

The Mechanics of Cash Value Growth in Whole Life Insurance

The cash value in a whole life insurance policy is a living benefit that accumulates over time. It’s designed to grow on a tax-deferred basis, meaning you don’t pay taxes on the growth each year. Taxes are only due when you withdraw funds or surrender the policy, and even then, withdrawals are typically limited to the amount of premiums paid in before incurring taxable gains. This tax-deferred growth is a significant advantage, allowing your money to compound more effectively over the long term compared to taxable investment accounts.

The growth rate of the cash value is determined by several factors. Firstly, the guaranteed interest rate stipulated in the policy contract provides a baseline. Secondly, if the policy is issued by a mutual insurance company and is “participating,” it may earn dividends. mutual company, you may also receive dividends, much like how you might research Cheap Auto Insurance Near Me. These dividends can be used in several ways: paid out in cash, used to reduce future premiums, left to accumulate with interest, or used to purchase additional paid-up insurance. When dividends are used to purchase paid-up additions, they effectively increase both the death benefit and the cash value of the policy, accelerating the growth of your whole life insurance investment.

Guaranteed Growth vs. Nonguaranteed Dividends

It’s essential to differentiate between the guaranteed growth and nonguaranteed dividends within a whole life insurance policy. The guaranteed interest rate is a contractual promise from the insurer, offering a foundational level of security. This means that even in adverse economic conditions, your cash value is assured to grow by at least this specified rate. This predictability is a cornerstone of the whole life insurance investment strategy, providing a sense of financial certainty.

Nonguaranteed dividends, on the other hand, represent a share of the insurer’s surplus earnings. These are influenced by the company’s investment performance, mortality experience, and operating expenses. While not guaranteed, dividends have historically been a significant component of the overall return for many participating whole life policies. The ability to reinvest these dividends to purchase additional paid-up insurance is a powerful way to enhance the long-term growth of your whole life insurance investment, effectively creating a snowball effect for both cash value and death benefit.

Accessing Your Whole Life Insurance Cash Value

One of the most attractive features of whole life insurance as an investment is the accessibility of its cash value. This accumulated sum is not locked away; it can be accessed during the policyholder’s lifetime. There are several primary methods for accessing these funds, each with its own implications for the policy’s death benefit and tax status.

The most common ways to access cash value include policy loans, withdrawals, and surrendering the policy. Policy loans allow you to borrow against your cash value, typically at a competitive interest rate. Importantly, policy loans are not considered taxable income, and you can repay them at your convenience. However, any outstanding loan balance, plus accrued interest, will reduce the death benefit paid to your beneficiaries upon your passing. Withdrawals, on the other hand, are permanent reductions of your cash value and death benefit. Withdrawals up to the policy’s basis (the total premiums paid) are generally tax-free. Amounts exceeding the basis are subject to ordinary income tax. Surrendering the policy means terminating the contract entirely, in which case you receive the surrender value of the cash value, less any surrender charges, and the death benefit ceases.

Policy Loans: A Tax-Advantaged Way to Access Funds

Policy loans are a particularly attractive feature of whole life insurance investment for liquidity needs. When you take a loan against your cash value, you are essentially borrowing from the insurance company using your policy’s cash value as collateral. The key advantage here is that these loans are generally not taxable. This makes them a flexible and often tax-efficient way to access funds for various purposes, such as education expenses, emergencies, or even as a supplement to retirement income, without triggering immediate tax liabilities.

The interest rate on policy loans is set by the insurance company and is typically competitive. It’s crucial to understand that while the loan itself is not taxed, any outstanding loan balance, including accrued interest, will reduce the death benefit payable to your beneficiaries. If the loan balance and interest exceed the cash value, the policy could lapse, potentially triggering a taxable event. Therefore, strategic management and understanding of loan terms are vital when using policy loans as part of your whole life insurance investment strategy.

Withdrawals and Surrender: Understanding the Implications

Withdrawals offer another avenue to access the accumulated cash value. When you make a withdrawal, you are permanently reducing both your cash value and your death benefit. The tax implications of withdrawals depend on the policy’s basis. Withdrawals up to the total amount of premiums paid into the policy are generally considered a return of principal and are tax-free. Any amount withdrawn in excess of the basis is treated as taxable income in the year of withdrawal.

Surrendering a whole life insurance policy is the most drastic way to access cash value, as it terminates the policy entirely. You receive the surrender value, which is the cash value less any applicable surrender charges. Surrender charges are typically higher in the early years of the policy and decrease over time. Similar to withdrawals, if the surrender value exceeds the total premiums paid, the gain is considered taxable income. Surrendering a policy also means forfeiting the death benefit and any future cash value accumulation, which can have significant long-term financial planning consequences.

Whole Life Insurance as a Component of a Diversified Portfolio

Integrating whole life insurance into a broader financial plan requires viewing it not as a standalone investment but as a complementary asset. Its unique characteristics – guaranteed cash value growth, tax deferral, lifelong protection, and access to liquidity – can provide a stable foundation within a diversified portfolio. For individuals who have maximized contributions to other tax-advantaged retirement accounts or are seeking to mitigate market risk, whole life insurance can play a valuable role.

The predictability of whole life insurance investment stands in contrast to the volatility of equity markets. While stocks and bonds offer the potential for higher returns, they also carry greater risk. Whole life insurance, with its guaranteed components, can act as a ballast, offering a secure place for a portion of one’s wealth. This can be particularly appealing for those nearing retirement who wish to preserve capital and ensure a guaranteed source of funds, regardless of market fluctuations. It’s about creating a balanced approach where different asset classes serve distinct purposes within the overall financial architecture.

Balancing Risk and Return

The primary appeal of whole life insurance as an investment lies in its balanced approach to risk and return. Unlike market-linked investments, the guaranteed cash value growth and death benefit provide a level of certainty that is difficult to find elsewhere. This risk mitigation is a key differentiator. While the returns on whole life insurance may not match the aggressive growth potential of some market investments, they are often more stable and predictable, especially when considering the long-term horizon.

For individuals who are risk-averse or have a low tolerance for market downturns, whole life insurance offers a compelling solution. It provides a guaranteed rate of return on the cash value, ensuring that your money grows steadily over time. This predictable growth, combined with the tax-deferred nature of the cash value, can lead to significant wealth accumulation without the anxiety associated with market volatility. It’s a tool for steady, reliable progress in building long-term financial security.

Long-Term Wealth Accumulation and Estate Planning

Whole life insurance is inherently a long-term financial instrument, making it exceptionally well-suited for long-term wealth accumulation and estate planning. The cash value grows over decades, benefiting from compounding interest and potential dividends. This sustained growth, coupled with the tax-deferred nature of the accumulation, can create a substantial asset over the policyholder’s lifetime.

Furthermore, the death benefit provided by whole life insurance is typically received by beneficiaries income-tax-free. This makes it a powerful tool for estate planning, allowing individuals to leave a legacy for their loved ones, cover estate taxes, or provide for charitable contributions. The cash value can also be used to pay for estate settlement costs, ensuring that other assets are not prematurely liquidated to meet these obligations. When considering the entirety of its benefits, whole life insurance investment stands out as a multifaceted tool for securing both personal financial well-being and the financial future of one’s heirs.

Choosing the Right Whole Life Insurance Policy

Selecting the appropriate whole life insurance policy is a critical step in leveraging its investment potential. Not all policies are created equal, and understanding the nuances of different offerings is paramount. Key factors to consider include the financial strength of the issuing insurance company, the policy’s dividend history (for participating policies), the guaranteed interest rate, policy fees and expenses, and riders that can be added to customize coverage.

Working with a knowledgeable insurance advisor who specializes in life insurance can be invaluable. They can help you navigate the complexities of policy illustrations, explain the various features and benefits, and assess which policy best aligns with your financial goals and risk tolerance. It’s a process that requires careful consideration and an understanding of your long-term objectives.

Evaluating Insurance Company Financial Strength

The long-term viability and performance of a whole life insurance policy are directly tied to the financial strength of the insurance company issuing it. Since these are long-term contracts, it’s crucial to partner with an insurer that has a robust financial standing and a history of stability. Reputable rating agencies such as A.M. Best, Standard & Poor’s, Moody’s, and Fitch provide ratings that assess an insurer’s ability to meet its financial obligations.

When evaluating companies, look for high ratings (e.g., A++ or AAA) from these agencies. A financially strong insurer is more likely to pay dividends consistently (if applicable), maintain its guaranteed rates, and fulfill its promises for the duration of the policy. This due diligence is a foundational element of making a sound whole life insurance investment decision.

Understanding Policy Fees and Expenses

Like any financial product, whole life insurance policies come with associated fees and expenses. These are typically embedded within the premiums and can impact the net growth of the cash value. Common expenses include administrative fees, cost of insurance charges (which cover the death benefit protection), and surrender charges (if the policy is surrendered early).

It’s vital to thoroughly review the policy’s fee structure and understand how these expenses are applied. High fees can erode the returns on your cash value, especially in the early years of the policy. Policy illustrations should clearly outline these costs. A transparent insurer will provide a detailed breakdown of all charges, allowing you to make an informed assessment of the policy’s long-term value as a whole life insurance investment.

The Role of Dividends in Enhancing Whole Life Insurance Investment Returns

For policies issued by mutual insurance companies that are classified as “participating,” dividends play a significant role in enhancing the overall returns of a whole life insurance investment. Dividends are essentially a share of the insurer’s profits distributed to policyholders. While not guaranteed, they have historically been a consistent source of added value for many policy owners.

The way dividends are used can further amplify the growth of your cash value and death benefit. Common dividend options include receiving them as cash, using them to reduce future premiums, letting them accumulate with interest, or purchasing additional paid-up insurance. Utilizing dividends to purchase paid-up additions is a powerful strategy for accelerating the growth of your whole life insurance investment, as each paid-up addition increases both the cash value and the death benefit on a tax-deferred basis.

Dividend Options and Their Impact

Policyholders typically have several options for how they want their dividends to be applied. Each option has a different impact on the policy’s growth and the immediate benefit to the policyholder. Understanding these choices is key to maximizing the benefit of whole life insurance investment.

- Cash Payment: The simplest option is to receive dividends as a direct cash payment. This provides immediate liquidity but does not contribute to the long-term growth of the cash value or death benefit.

- Reduce Premiums: Dividends can be used to offset future premium payments, effectively lowering the out-of-pocket cost of maintaining the policy. This is a practical way to manage ongoing expenses.

- Accumulate with Interest: Dividends can be left with the insurance company to earn interest, further growing the cash value on a tax-deferred basis.

- Purchase Paid-Up Additions (PUAs): This is often considered the most beneficial option for long-term wealth accumulation. Dividends are used to purchase small, fully paid-up life insurance policies. Each PUA increases both the policy’s cash value and its death benefit, and the PUA itself starts earning cash value and potentially dividends immediately. This strategy effectively “supercharges” the growth of your whole life insurance investment.

Illustrative Example of Dividend Reinvestment

To illustrate the power of dividend reinvestment, consider a hypothetical scenario. Suppose a policyholder pays $10,000 annually in premiums for a whole life policy. In the early years, a portion of this premium goes towards the cost of insurance and administrative fees, with the remainder building cash value. If the policy pays a dividend of $1,000 in year five, and the policyholder chooses to use this dividend to purchase paid-up additions, this $1,000 effectively buys more insurance that immediately adds to the cash value and increases the death benefit. Over decades, as dividends continue to be reinvested, this compounding effect can significantly enhance the policy’s overall value, demonstrating a robust whole life insurance investment growth trajectory.

Who Benefits Most from Whole Life Insurance Investment?

Whole life insurance is not a universal solution, but it can be a powerful tool for specific individuals and financial situations. Those who benefit most are typically individuals seeking long-term financial security, tax-advantaged growth, and a guaranteed death benefit. This often includes individuals with a moderate to high net worth who have already maximized other tax-advantaged retirement savings vehicles, such as 401(k)s and IRAs.

It’s also an attractive option for those who are risk-averse and prioritize capital preservation over speculative growth. The predictable nature of the cash value accumulation and the guaranteed death benefit provide a sense of financial stability. Furthermore, individuals focused on estate planning and leaving a legacy for their beneficiaries often find whole life insurance to be an indispensable component of their strategy. The tax-free nature of the death benefit and the ability to use the cash value for estate liquidity are significant advantages.

High-Income Earners and Maxed-Out Retirement Accounts

For high-income earners who have diligently contributed to their 401(k)s, IRAs, and other retirement plans, the annual contribution limits can become a constraint. When these avenues for tax-advantaged savings are exhausted, they often look for alternative methods to grow their wealth tax-efficiently. Whole life insurance offers a compelling solution in this regard. The cash value grows tax-deferred, and access to these funds through policy loans is generally tax-free, providing a valuable supplemental savings and investment vehicle.

Moreover, the death benefit component of whole life insurance remains a crucial element for high-net-worth individuals. It ensures that a substantial sum is available to their beneficiaries, often free of income tax, which can be particularly beneficial for estate planning and wealth transfer. This combination of tax-advantaged growth and a guaranteed death benefit makes whole life insurance an attractive proposition for this demographic.

Individuals Focused on Estate Planning and Legacy Building

Estate planning is a critical aspect of financial management, especially for those with significant assets. Whole life insurance plays a pivotal role in this area by providing a guaranteed death benefit that can be passed on to heirs, often income-tax-free. This ensures that loved ones are provided for and that a legacy can be established without diminishing other assets intended for distribution.

The cash value within the policy can also be utilized to address estate liquidity needs. For instance, it can be used to pay estate taxes, funeral expenses, or other final costs, preventing the forced sale of other assets at potentially unfavorable times. By strategically incorporating whole life insurance into an estate plan, individuals can ensure a smoother transition of wealth and provide significant financial support for future generations, solidifying its position as a valuable whole life insurance investment for legacy building.

Comparing Whole Life Insurance Investment to Other Investment Options

To fully appreciate the role of whole life insurance as an investment, it’s beneficial to compare it with other common financial vehicles. Its unique blend of protection and growth differentiates it significantly from pure investment products like stocks, bonds, or mutual funds, as well as other insurance products such as term life insurance or variable universal life insurance.

While stocks and bonds offer higher potential returns, they also come with greater market risk and volatility. Term life insurance, on the other hand, provides pure death benefit protection for a specified period but lacks any cash value accumulation or investment component. Variable universal life insurance, while offering investment potential through sub-accounts, carries market risk and can be more complex to manage. Whole life insurance, with its guaranteed cash value growth and predictable returns, occupies a distinct niche, offering a stable, long-term approach to wealth building and protection.

Whole Life vs. Term Life Insurance

The fundamental difference between whole life and term life insurance lies in their purpose and duration. Term life insurance is designed to provide coverage for a specific period, typically 10, 20, or 30 years. It offers a death benefit if the insured dies within that term, but it has no cash value component and is generally less expensive than whole life insurance for the same death benefit amount. It’s purely a death protection product.

Whole life insurance, conversely, provides lifelong coverage and includes a cash value component that grows over time on a tax-deferred basis. While the premiums for whole life are higher than for term life, the cash value accumulation, guaranteed growth, and potential for dividends make it a financial planning tool beyond just death benefit protection. For those looking for a death benefit and a savings vehicle in one, whole life insurance investment offers a more comprehensive solution.

Whole Life vs. Indexed Universal Life (IUL) and Variable Universal Life (VUL)

Indexed Universal Life (IUL) and Variable Universal Life (VUL) policies offer more flexible premiums and death benefits than traditional whole life. IUL policies link their cash value growth to a market index (like the S&P 500), offering potential for higher returns than whole life but with caps and participation rates, and often with a floor to prevent losses. VUL policies allow policyholders to invest cash value in sub-accounts, similar to mutual funds, offering the highest potential for growth but also exposing the cash value to significant market risk.

Whole life insurance, in contrast, provides guaranteed cash value growth and a guaranteed death benefit, offering a level of predictability that IUL and VUL policies do not. While IUL and VUL can offer higher potential returns, they also carry more risk and complexity. Whole life insurance investment prioritizes stability and guaranteed growth, making it a more conservative choice for those who value certainty over market speculation. Similarly, you should also Compare Car Insurance Rates to ensure your overall financial protection remains balanced. The simplicity and guarantees of whole life are often its strongest selling points for a segment of the market.

Key Considerations for Utilizing Whole Life Insurance as an Investment

When considering whole life insurance as an investment, several key factors must be thoroughly evaluated to ensure it aligns with your financial objectives and risk tolerance. It’s not a decision to be made lightly, as these policies are long-term commitments. Understanding the structure, costs, and benefits is paramount to making an informed choice.

The duration of the policy, the financial strength of the insurer, the specific riders and features, and how the policy integrates with your overall financial plan are all critical elements. Furthermore, it’s important to have realistic expectations regarding returns; whole life insurance is generally not designed for rapid wealth creation but rather for steady, secure, and long-term accumulation and protection.

Long-Term Commitment and Policy Structure

Whole life insurance is fundamentally a long-term contract. Policies are designed to last for the insured’s entire lifetime, provided premiums are paid. This long-term commitment means that the benefits, particularly the cash value growth, become more substantial and efficient over many years. Early surrender of a whole life policy can result in significant financial penalties and loss of accumulated value.

The structure of the policy, including the premium payment schedule and the guaranteed cash value growth rate, is predetermined. While some policies offer limited flexibility in premium payments, the core structure is designed for stability. Understanding this long-term commitment is crucial for anyone considering whole life insurance investment, as it requires a disciplined approach to premium payments and a long-term perspective on financial growth.

Realistic Return Expectations

It is essential to set realistic expectations regarding the returns generated by whole life insurance. While the cash value grows tax-deferred and may earn dividends, the rates of return are typically more conservative compared to market-driven investments like stocks or mutual funds. The guaranteed interest rate provides a floor, but it is often modest.

The true value of whole life insurance investment often lies in its combination of guaranteed growth, tax deferral, lifelong protection, and the potential for dividends, rather than solely on aggressive growth. For individuals seeking a secure, predictable way to build wealth over the long term, and who are willing to accept more moderate returns in exchange for reduced risk and guaranteed benefits, whole life insurance can be an excellent choice. It’s about financial stability and certainty as much as it is about accumulation.