Whole Life Insurance Investment – Imagine a financial tool that doesn’t just offer a safety net for your loved ones but also grows with you over time, accumulating value and potentially providing a source of funds when you need it most. This is the essence of whole life insurance as an investment. Far from being solely a death benefit, this type of permanent life insurance policy is designed to offer a dual purpose: lifelong protection and a cash value component that builds wealth. It’s a concept that often sparks curiosity, as it blends the security of insurance with the potential rewards of an investment, presenting a unique avenue for long-term financial planning.

At its core, whole life insurance investment functions by allocating a portion of your premium payments towards building a cash value that grows on a tax-deferred basis. This isn’t a volatile stock market investment; rather, it’s a more predictable, guaranteed growth mechanism. Over the years, this cash value can increase, offering a tangible asset that can be accessed through policy loans or withdrawals. This feature transforms the policy from a pure expense into a financial resource that can be leveraged for various life events, from funding retirement to covering unexpected expenses, all while maintaining the primary death benefit for your beneficiaries.

The appeal of whole life insurance as an investment lies in its inherent guarantees and long-term perspective. Unlike term life insurance, which expires after a set period, whole life policies are designed to last your entire lifetime, providing continuous coverage. Coupled with the guaranteed cash value growth and potential for dividends , it offers a stable, albeit often slower-paced, path to wealth accumulation. Further details are available in Cheap Auto Insurance Near Me. This makes it an attractive option for individuals seeking a predictable and secure way to integrate insurance protection with their broader financial and estate planning goals, offering a sense of control and foresight in managing their financial future.

Whole Life Insurance Investment

Whole life insurance, often perceived solely as a death benefit product, can indeed function as a sophisticated investment vehicle, particularly when viewed through the lens of its cash value accumulation component. This form of permanent life insurance offers lifelong coverage and, crucially, builds a tax-deferred cash value over time. Understanding the intricacies of this cash value is paramount to appreciating its investment potential.

The Mechanics of Cash Value Accumulation in Whole Life Insurance

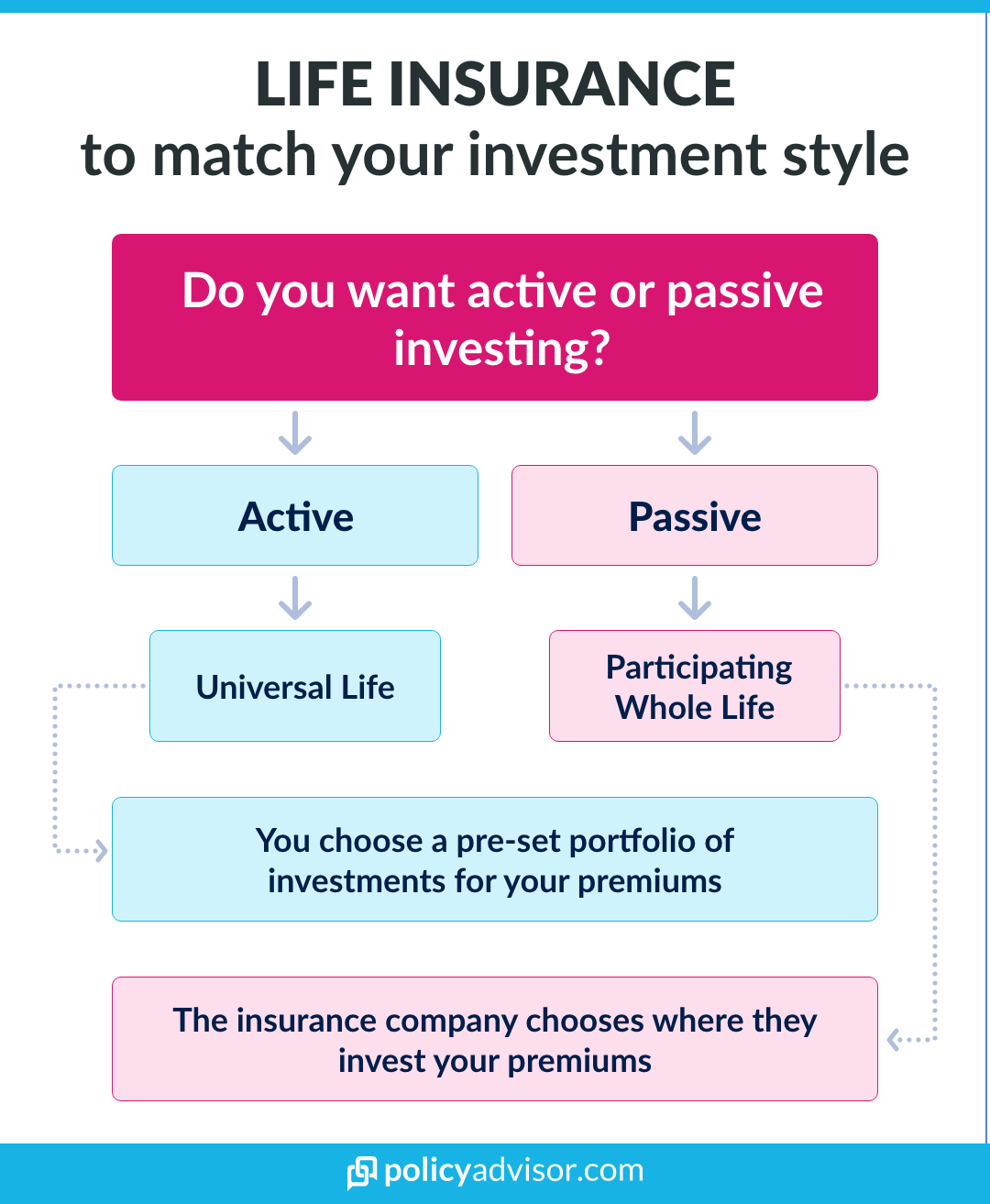

When you pay premiums for a whole life insurance policy, a portion of that premium goes towards the cost of insurance (to cover the death benefit), administrative expenses, and the remaining portion is allocated to the policy’s cash value. This cash value grows on a tax-deferred basis, meaning you don’t pay taxes on the earnings each year. The growth is typically guaranteed by the insurance company, often at a fixed rate, and may also include non-guaranteed dividends if the policy is issued by a mutual insurance company. These dividends can be used in several ways, further enhancing the investment aspect of whole life insurance.

Guaranteed Growth and Potential Dividends

The guaranteed cash value growth provides a stable, predictable component to your whole life insurance investment. This inherent stability is a significant differentiator compared to more volatile market-based investments. Beyond the guaranteed rate, participating policies (those eligible for dividends) offer the potential for additional growth. Dividends are a share of the insurance company’s profits, and when paid, they can be used to:

- Purchase additional paid-up insurance, increasing both the death benefit and the cash value.

- Be taken as cash, reducing the out-of-pocket cost of premiums or providing a source of funds.

- Be left with the insurer to accumulate interest, further boosting the cash value.

- Be used to pay future premiums.

This flexibility in dividend usage allows policyholders to tailor the growth and benefits of their whole life insurance investment to their evolving financial needs.

Accessing Your Whole Life Insurance Investment: Loans and Withdrawals

One of the key advantages of the cash value component in whole life insurance as an investment is the ability to access these funds without triggering immediate tax consequences. There are two primary methods: policy loans and withdrawals.

Policy Loans

When you take a loan against your whole life insurance policy, you are borrowing against the accumulated cash value. The loan amount, plus interest, is deducted from the death benefit if the loan is not repaid. A significant benefit of policy loans is that they are generally not taxable, even if the loan amount exceeds the premiums paid. The interest on the loan is paid to the insurance company, and the loan balance reduces the amount of cash value available for growth and as collateral. It’s crucial to understand the loan interest rate and how it impacts the policy’s performance. Unpaid loans, along with accrued interest, will reduce the death benefit and can eventually cause the policy to lapse if the loan balance equals or exceeds the cash value.

Withdrawals

You can also make withdrawals from the cash value of your whole life insurance policy. Withdrawals are typically treated as a return of premium first, meaning they are tax-free up to the amount of premiums you’ve paid into the policy. Once the withdrawals exceed the total premiums paid, the earnings portion of the withdrawal becomes taxable as ordinary income. It’s important to note that withdrawals reduce both the cash value and the death benefit of the policy. Therefore, careful consideration is needed to ensure that withdrawals do not jeopardize the long-term insurability or the intended death benefit.

Whole Life Insurance Investment vs. Other Investment Vehicles

Comparing whole life insurance investment to other common investment strategies requires a nuanced understanding of risk, return, and time horizon.

Comparison with Term Life Insurance and Pure Investment Strategies

Term life insurance provides coverage for a specific period and does not build cash value. While it is typically much less expensive than whole life insurance, it offers no investment component. Pure investment strategies, such as stocks, bonds, or mutual funds, offer the potential for higher returns but also carry greater market risk and immediate tax implications on gains. Whole life insurance investment offers a blend: a guaranteed death benefit, tax-deferred cash value growth with some level of guaranteed return, and tax-advantaged access to funds.

Tax Advantages of Whole Life Insurance Investment

The tax-deferred growth of the cash value is a significant advantage. This means your investment earnings compound over time without being diminished by annual taxes. Furthermore, the death benefit paid to beneficiaries is generally income tax-free. When comparing the net, after-tax returns, whole life insurance investment can be competitive, especially for individuals in higher tax brackets or those looking for a stable, long-term financial asset.

Strategic Uses of Whole Life Insurance as an Investment

The strategic application of whole life insurance as an investment extends beyond simple wealth accumulation. It can be a powerful tool for estate planning, business succession, and even charitable giving.

Estate Planning and Wealth Transfer

For individuals with significant estates, whole life insurance can be an invaluable tool for estate planning. The tax-free death benefit can provide liquidity to pay estate taxes, preventing the forced sale of other assets. It can also be used to equalize inheritances among heirs, providing a substantial, tax-free sum to one heir while other assets are distributed differently. The cash value itself can also be passed on to beneficiaries.

Business Succession Planning

In closely held businesses, whole life insurance can fund buy-sell agreements. A policy owned by the business on a key owner’s life can provide the funds needed for the remaining owners to purchase the deceased owner’s share from their estate, ensuring business continuity. Key person insurance, also often structured as whole life, can provide a financial cushion to the business in the event of the death of a crucial employee.

Charitable Giving Strategies

Whole life insurance can also be incorporated into charitable giving plans. A policy can be gifted to a charity, with the charity named as the beneficiary. Over time, the cash value can grow, and upon the insured’s death, the death benefit provides a substantial gift to the charity. Alternatively, an individual can purchase a policy and name a charity as the beneficiary, allowing their legacy to continue to support their chosen cause.

Considerations and Potential Drawbacks of Whole Life Insurance Investment

While whole life insurance investment offers compelling benefits, it’s not a one-size-fits-all solution. Several factors warrant careful consideration.

Higher Premiums Compared to Term Life

The cost of whole life insurance premiums is significantly higher than that of term life insurance. This is due to the lifelong coverage and the cash value accumulation component. Prospective policyholders must assess whether they can comfortably afford these higher premiums over the long term.

Lower Liquidity in Early Years

The cash value in a whole life insurance policy grows gradually. In the initial years, the cash surrender value (the amount you would receive if you canceled the policy) is typically less than the total premiums paid. This means that accessing funds in the early stages of the policy can result in a loss. This makes it less suitable for short-term savings goals or emergency funds.

Complexity and Fees

Whole life insurance policies can be complex instruments, and understanding all the nuances of the contract, including fees, charges, and the way cash value is calculated, is crucial. It’s essential to work with a knowledgeable advisor who can clearly explain these elements. Some policies may have surrender charges if the policy is canceled within a certain period.

Choosing the Right Whole Life Insurance Investment Policy

Selecting the appropriate whole life insurance policy requires careful due diligence and an understanding of your personal financial objectives.

Working with a Qualified Insurance Professional

It is highly recommended to consult with a licensed and experienced insurance agent or financial advisor who specializes in permanent life insurance. They can help you assess your needs, explain different policy options, and guide you through the application process. Look for professionals who are transparent about commissions and fees and prioritize finding the best fit for your situation, not just the product with the highest commission.

Understanding Policy Illustrations

Insurance companies provide policy illustrations that project the future performance of the cash value and death benefit. These illustrations often show both guaranteed and non-guaranteed (dividend) scenarios. It’s important to understand the assumptions behind these illustrations and to not rely solely on the most optimistic projections. Focus on the guaranteed values and consider the non-guaranteed elements as potential bonuses.

The Role of Whole Life Insurance Investment in a Diversified Portfolio

Whole life insurance investment can play a valuable role within a well-diversified financial portfolio, offering a unique combination of protection, stability, and tax advantages that complement other investment strategies. It’s not meant to be the sole component of a portfolio but rather a strategic addition that addresses specific financial planning needs, particularly those related to long-term security, wealth transfer, and tax efficiency. When integrated thoughtfully, whole life insurance investment can contribute significantly to overall financial well-being.