Workers Compensation Insurance Cost – For any business owner, understanding the various costs associated with operating a successful enterprise is paramount. Among these, workers’ compensation insurance stands out as a crucial, yet often complex, expense. This type of insurance is not merely a regulatory requirement in most jurisdictions; it serves as a vital safety net, protecting both employees from the financial burdens of work-related injuries or illnesses and employers from potentially crippling lawsuits and medical costs. The intricacies of how these costs are determined can seem daunting, but a clear grasp of the underlying factors is essential for effective financial planning and risk management.

At its core, workers’ compensation insurance cost is a reflection of the perceived risk associated with a particular business and its employees. Insurers analyze a multitude of data points to calculate premiums, with the ultimate goal of balancing the potential for claims against the revenue generated by the business. This calculation is far from arbitrary; it involves a sophisticated assessment of industry classifications, historical claims data, payroll figures, and even the specific safety practices implemented by an employer. Understanding these components is the first step for any business owner looking to manage or even reduce their insurance expenditures.

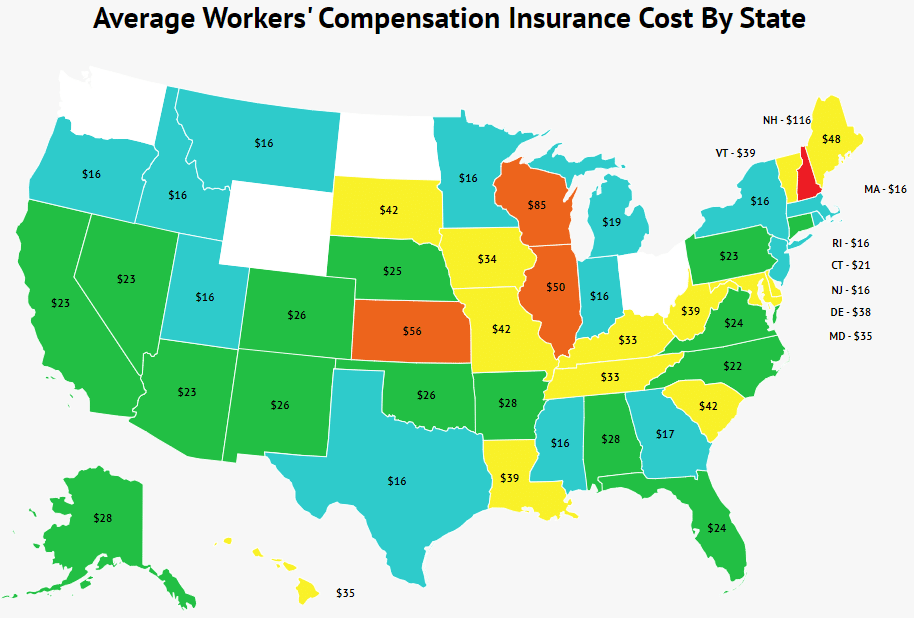

The journey to deciphering workers’ compensation insurance costs begins with recognizing that it’s a dynamic figure, influenced by ongoing business operations and external economic factors. Whether you’re a small startup or an established corporation, the premium you pay will be a direct consequence of the inherent hazards of your industry, the number of employees you have, and their respective wages. Furthermore, an employer’s commitment to workplace safety and their past claims history play a significant role in shaping the final cost. A reliable reference on this topic is Business Liability Insurance Cost. Navigating this landscape requires a proactive approach, focusing on risk mitigation and informed decision-making to ensure that this essential insurance expense is both adequate and economically viable.

# Workers Compensation Insurance Cost The cost of workers’ compensation insurance is a critical consideration for businesses of all sizes. Understanding the factors that influence these costs, how premiums are calculated, and strategies for managing expenses can significantly impact a company’s bottom line. This in-depth exploration delves into the intricacies of workers’ compensation insurance cost, providing a comprehensive overview for employers. ## Understanding the Fundamentals of Workers’ Compensation Insurance Cost Workers’ compensation insurance is a no-fault system designed to protect employees who suffer work-related injuries or illnesses. It provides benefits such as medical treatment, lost wages, and rehabilitation services. For employers, it offers protection against lawsuits from injured employees, ensuring a predictable cost for these benefits. The workers’ compensation insurance cost is not static; it is a dynamic figure influenced by a multitude of variables specific to each business. ### Key Components Influencing Workers’ Compensation Insurance Cost Several core elements contribute to the overall workers’ compensation insurance cost for a business. These are meticulously assessed by insurance carriers to determine the appropriate premium. #### 1. Classification Codes (NCCI Codes or State-Specific Codes) This is arguably the most significant factor in determining workers’ compensation insurance cost. Every job classification within a business is assigned a specific code, which represents the inherent risk associated with that type of work. For instance, an office worker typically has a much lower risk profile than a construction worker. High-Risk Classifications: Jobs involving manual labor, operation of heavy machinery, exposure to hazardous materials, or work at heights generally fall into high-risk categories. These classifications will have higher premium rates per $100 of payroll. Low-Risk Classifications: Office-based roles, administrative positions, and jobs with minimal physical exertion are considered low-risk and will have lower premium rates. Multiple Classifications: Businesses often have employees in various roles, meaning multiple classification codes will be applied. The insurer will calculate the premium for each classification based on the payroll allocated to that specific job type. #### 2. Payroll Payroll is a primary driver of workers’ compensation insurance cost. Premiums are typically calculated as a rate per $100 of an employee’s annual wages. Therefore, businesses with higher overall payroll will generally have higher workers’ compensation insurance costs, assuming all other factors remain constant. Exclusions: Some states allow for the exclusion of certain employee types from workers’ compensation coverage, such as corporate officers or sole proprietors, which can impact the total payroll used for premium calculation. Varying Rates: The rate applied to payroll is not uniform across all employees. It is specific to the classification code assigned to their job. #### 3. Experience Modification Factor (eMod) The experience modification factor, often referred to as the “eMod” or “X-Mod,” is a crucial element that adjusts a business’s premium based on its past claims history compared to the average for similar businesses. It is a powerful tool for influencing workers’ compensation insurance cost. eMod Below 1.00 (Credit): A factor below 1.00 indicates that the business has had fewer claims or lower claim costs than the industry average. This results in a premium credit, lowering the overall workers’ compensation insurance cost. eMod Above 1.00 (Debit): A factor above 1.00 signifies a worse-than-average claims history, leading to a premium surcharge and an increase in workers’ compensation insurance cost. eMod of 1.00 (Neutral): This means the business’s claims history aligns with the industry average. Calculation: The eMod is calculated by an independent rating bureau (like the NCCI in most states) based on a rolling three-year period of a company’s claims data, excluding the most recent full year. The formula considers the expected losses versus the actual losses. #### 4. State Regulations and Governing Laws Workers’ compensation is regulated at the state level, and each state has its own laws, benefit levels, and rating bureaus. This means that the workers’ compensation insurance cost can vary significantly from one state to another, even for businesses with identical operations and employee profiles. Benefit Levels: States with more generous benefits for injured workers will generally have higher premium costs. Dispute Resolution: The ease or difficulty of resolving workers’ compensation claims within a state can also impact costs. Monopolistic States: A few states (e.g., North Dakota, Ohio, Washington, Wyoming) operate monopolistic state funds, meaning employers must purchase workers’ compensation insurance through the state. Private insurers are not permitted to offer this coverage in these states. #### 5. Safety Record and Loss Control Efforts A proactive approach to workplace safety can directly reduce workers’ compensation insurance cost. Insurers reward businesses that demonstrate a commitment to preventing accidents and injuries. Safety Programs: Implementing comprehensive safety programs, providing regular training, and conducting workplace hazard assessments are vital. Claims Management: Effective claims management, including prompt reporting of injuries, thorough investigation, and facilitating employee return-to-work, can significantly reduce the overall cost of claims and, consequently, the premium. Return-to-Work Programs: Successful return-to-work programs help injured employees get back to their jobs sooner, reducing the duration of lost wages and medical expenses, which in turn positively impacts the eMod and workers’ compensation insurance cost. ## How Workers’ Compensation Insurance Premiums Are Calculated The calculation of a workers’ compensation insurance premium is a multi-step process that combines the factors discussed above. While the exact formulas can be complex and vary by state and insurer, the general methodology remains consistent. ### The Basic Premium Calculation Formula The fundamental formula for calculating a preliminary premium is: (Payroll per Classification Code / 100) Rate per Classification Code = Base Premium for Classification This is then summed up for all classification codes. ### Applying the Experience Modification Factor Once the total base premium is determined, the eMod is applied: Total Base Premium Experience Modification Factor = Adjusted Premium ### Additional Factors and Surcharges/Credits Beyond the eMod, other factors can further adjust the premium: Schedule Rating: This is an individualized adjustment that can be applied to a business’s premium based on specific workplace conditions, safety measures, or the nature of the business that are not fully captured by the classification codes or eMod. It can result in a debit (increase) or credit (decrease) to the premium. Large Deductible Plans: Some policies allow employers to choose a deductible for each claim. The employer pays this deductible amount directly, and the insurer covers the rest. Choosing a larger deductible can significantly reduce the workers’ compensation insurance cost, but it requires the employer to have the financial capacity to cover potential deductible payments. Loss Sensitive Plans: These plans, such as Retrospective Rating, adjust premiums retroactively based on the actual claims experience during the policy period. They are typically for larger employers and can lead to significant savings if claims are well-managed, but also carry the risk of higher premiums if claims are frequent or severe. ## Strategies for Managing and Reducing Workers’ Compensation Insurance Cost Understanding the drivers of workers’ compensation insurance cost is the first step; implementing strategies to reduce it is the next. Proactive management can lead to substantial savings over time. ### 1. Prioritize Workplace Safety This cannot be overstated. A strong safety culture is the most effective way to reduce claims and, consequently, lower workers’ compensation insurance cost. Develop and Enforce Safety Policies: Clearly written safety procedures for all tasks, with regular reinforcement and disciplinary action for non-compliance. Invest in Safety Training: Provide comprehensive and ongoing training for all employees, tailored to their specific roles and potential hazards. Conduct Regular Safety Inspections: Proactively identify and mitigate hazards before they lead to accidents. This includes equipment maintenance, proper storage of materials, and ergonomic assessments. Promote a Reporting Culture: Encourage employees to report near misses and potential hazards without fear of reprétailiation. This allows for intervention before an actual injury occurs. ### 2. Implement a Robust Return-to-Work Program A well-structured return-to-work program helps injured employees transition back to their jobs as quickly and safely as possible. Identify Modified Duty Options: Develop a list of light-duty or modified tasks that injured employees can perform while recovering. Communicate with Healthcare Providers: Maintain open communication with treating physicians to understand the employee’s work restrictions and capabilities. Facilitate a Smooth Transition: Ensure supervisors are aware of the employee’s return and their modified duties. ### 3. Optimize Classification Codes Ensure your business is accurately classified. Misclassification can lead to paying too much or too little, the latter of which can result in penalties. Review Job Duties Annually: Regularly assess the actual tasks employees perform and ensure they align with the assigned classification codes. Consult with Your Insurance Broker: Work with an experienced broker who can help identify potential misclassifications and advocate for correct coding with the insurer. ### 4. Manage Claims Effectively Prompt and efficient claims management can significantly mitigate the financial impact of injuries. Report Injuries Immediately: File claims as soon as possible after an injury occurs. Delays can complicate the process and increase costs. Investigate All Accidents: Conduct thorough investigations to understand the root cause of accidents and implement corrective actions. Stay Involved in the Claims Process: Monitor the progress of claims, communicate with adjusters, and ensure that appropriate medical treatment is being provided. ### 5. Negotiate with Insurers and Brokers Don’t be afraid to discuss your policy and costs with your insurance provider or broker. Shop Around: Obtain quotes from multiple insurance carriers regularly to compare pricing and coverage. Understand Your eMod: Regularly review your eMod calculation and understand how it is derived. If you believe there are errors, dispute them. Consider Different Policy Structures: Discuss options like large deductible plans or loss-sensitive programs with your broker if they are suitable for your business size and risk tolerance. ### 6. Employee Education and Engagement Educate your employees about the importance of safety and their role in preventing injuries. Engaged employees are more likely to follow safety protocols and contribute to a safer workplace. ## The Role of Insurance Brokers in Managing Workers’ Compensation Insurance Cost An experienced and knowledgeable insurance broker is an invaluable asset for businesses seeking to manage their workers’ compensation insurance cost. They act as an intermediary between the employer and insurance carriers, providing expertise and advocacy. ### Key Services Provided by Brokers: Risk Assessment: Helping businesses identify their unique risks and how they translate into workers’ compensation classifications and costs. Market Navigation: Accessing a wide range of insurance carriers and understanding their appetite for different types of businesses and risks. Quote Comparison: Obtaining and analyzing quotes from multiple insurers to find the best combination of coverage and price. Policy Review: Explaining policy terms, conditions, and endorsements to ensure the business has adequate coverage. Claims Advocacy: Assisting with the claims process, helping to resolve disputes, and ensuring claims are handled efficiently. Loss Control Consultation: Recommending and facilitating access to resources for improving workplace safety and reducing claims. eMod Analysis: Helping businesses understand their experience modification factor and identify potential errors or opportunities for improvement. ## Conclusion The workers’ compensation insurance cost is a complex but manageable aspect of business operations. By thoroughly understanding the factors that influence premiums, implementing robust safety and claims management programs, and leveraging the expertise of insurance professionals, businesses can effectively control and potentially reduce their expenses. A proactive approach to risk management is not just about saving money; it’s about creating a safer and more productive environment for all employees, which ultimately benefits the entire organization.