Restaurant Insurance Cost – Opening the doors to your dream restaurant is an exhilarating prospect, filled with culinary creativity and the promise of serving your community. Yet, beneath the veneer of delicious dishes and welcoming ambiance lies a crucial layer of protection that every restaurateur must consider: insurance. The cost of restaurant insurance is not a one-size-fits-all figure; it’s a complex equation influenced by a multitude of factors unique to your establishment. From the type of cuisine you serve to the square footage of your dining room and the number of employees on your payroll, each element plays a role in determining the premiums you’ll face.

Understanding these costs is paramount for sound financial planning and ensuring your business is adequately covered against unforeseen events. Without the right insurance, a single accident, a natural disaster, or a costly lawsuit could jeopardize everything you’ve worked so hard to build. Therefore, delving into the specifics of restaurant insurance cost isn’t just a bureaucratic necessity; it’s a strategic imperative. It allows you to budget effectively, compare quotes with confidence, and ultimately, secure a policy that provides peace of mind, letting you focus on what you do best – creating exceptional dining experiences.

This article aims to demystify the world of restaurant insurance costs, providing a clear overview of the key components that contribute to your overall premium. We’ll explore the different types of insurance policies commonly needed by restaurants, from general liability and liquor liability to workers’ compensation and property insurance. By breaking down these elements, you’ll gain a comprehensive understanding of where your insurance dollars are going and how you might be able to optimize your coverage while managing expenses. We will also examine the factors influencing your Business Liability Insurance Cost to help you budget effectively. Prepare to gain insights that will empower you to make informed decisions for the long-term health and security of your restaurant.

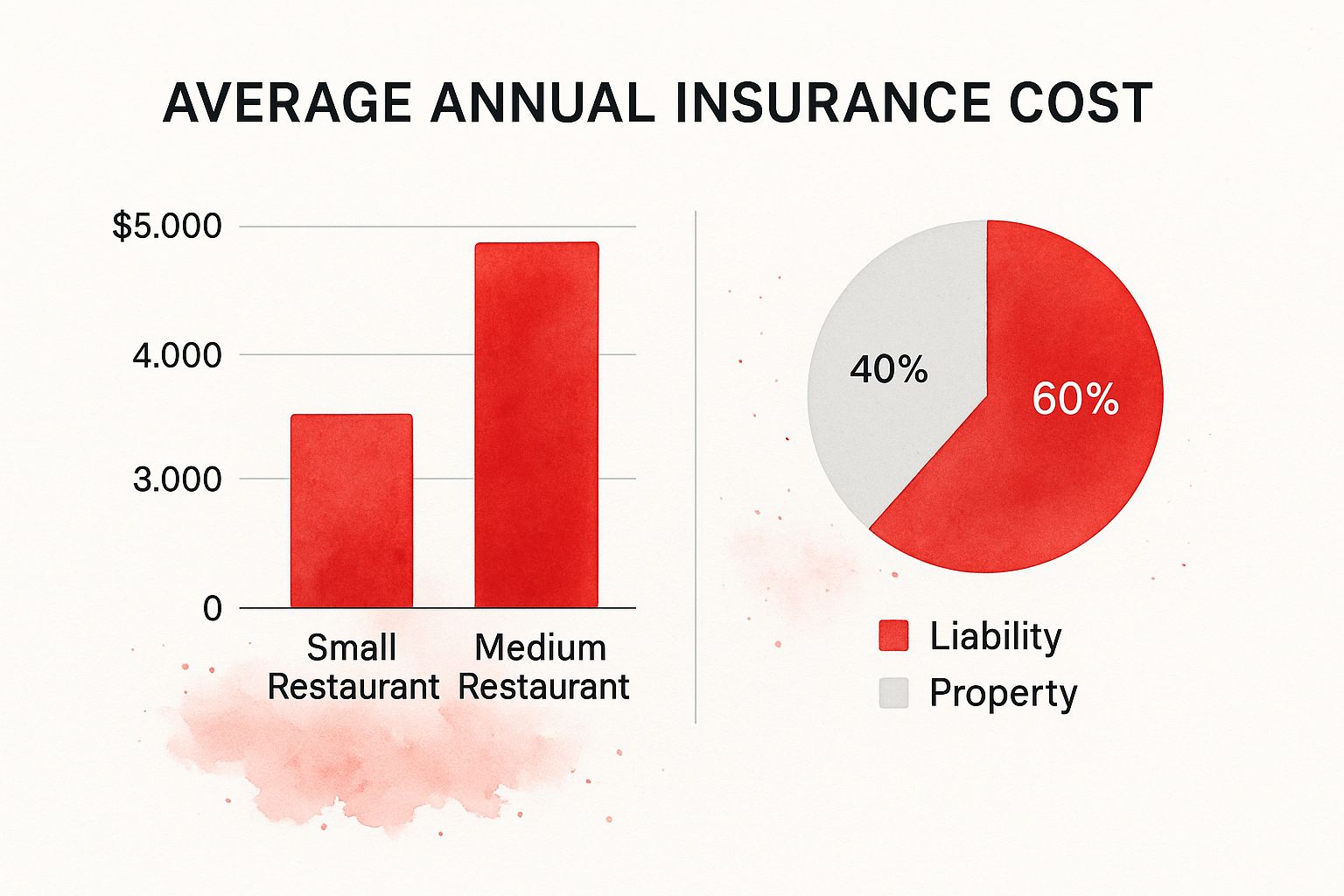

# Restaurant Insurance Cost Understanding the restaurant insurance cost is a critical undertaking for any restaurateur, whether you’re launching a new establishment or operating an established business. The financial outlay for insurance is not a static figure; it’s a dynamic calculation influenced by a multitude of factors that directly impact your bottom line. Navigating this complex landscape requires a detailed appreciation of what goes into determining your restaurant insurance cost, enabling you to secure appropriate coverage without overspending. This comprehensive guide aims to demystify the various components that contribute to your overall restaurant insurance cost, providing you with the knowledge to make informed decisions. ## Key Factors Influencing Restaurant Insurance Cost The price you’ll pay for restaurant insurance is not a one-size-fits-all proposition. Insurers meticulously assess a range of risks associated with your specific business to arrive at a personalized restaurant insurance cost. These factors can be broadly categorized, and a deep dive into each is essential for a thorough understanding. ### Location and Geographic Risk The geographical location of your restaurant plays a surprisingly significant role in its restaurant insurance cost. Areas prone to natural disasters such as earthquakes, hurricanes, floods, or even high crime rates will naturally command higher premiums. Insurers factor in the likelihood of property damage or business interruption due to these events. For instance, a restaurant situated in a coastal region with a history of severe storms will likely experience a higher restaurant insurance cost compared to one in a more geologically stable inland area. Furthermore, urban environments with higher rates of vandalism or theft might also see an increase in their restaurant insurance cost. ### Type and Size of Restaurant The nature of your culinary operations directly impacts the restaurant insurance cost. Different types of restaurants present unique risks. Fine Dining Restaurants: These establishments often have higher customer spending, more valuable equipment (e.g., specialized ovens, wine cellars), and a greater perceived risk of liquor liability claims due to serving premium alcohol. This can lead to a higher restaurant insurance cost. Fast Food Restaurants: While they might have lower per-customer value, the high volume of transactions and the potential for slip-and-fall accidents due to busy queues can influence the restaurant insurance cost. Cafes and Coffee Shops: Generally considered lower risk, but still subject to product liability for food and beverage consumption and general liability for customer accidents. The restaurant insurance cost here is typically more moderate. Bars and Nightclubs: These establishments carry a significantly higher risk of liquor liability claims, which is a major driver of their restaurant insurance cost. Fights, over-serving, and property damage are also key concerns. Catering Businesses: The risk profile shifts to include off-site operations, transportation of food, and potential issues with foodborne illnesses at events. This can impact the overall restaurant insurance cost. The physical size of your restaurant, measured in square footage, also contributes to the restaurant insurance cost. Larger spaces generally mean more property to insure, higher potential for accidents, and a greater number of employees, all of which can increase premiums. ### Revenue and Sales Volume Your restaurant’s annual revenue is a primary indicator of its overall exposure and the potential severity of a claim. A higher revenue typically translates to a higher restaurant insurance cost because it suggests more customers, more transactions, and greater potential for financial loss if something goes wrong. Insurers use revenue figures to gauge the scale of your operations and the potential payout in case of a liability claim or business interruption. ### Number of Employees The number of staff members you employ directly influences your restaurant insurance cost, particularly concerning workers’ compensation insurance. More employees mean a higher likelihood of workplace injuries. Employers’ liability, which covers legal costs if an employee sues for a work-related injury, is also a factor. The more employees you have, the greater the potential restaurant insurance cost associated with these coverages. ### Menu and Food Preparation The types of food you serve and how you prepare them can significantly affect your restaurant insurance cost. Restaurants that handle raw meats, seafood, or operate with complex cooking processes might face higher premiums due to an increased risk of foodborne illnesses or fires. Establishments that offer buffets, where food is exposed for longer periods, may also see a difference in their restaurant insurance cost. ### Alcohol Sales If your restaurant serves alcohol, this is a critical factor in determining your restaurant insurance cost. Liquor liability insurance is essential and can substantially increase your premiums. The more alcohol you sell, and the higher the alcohol content of your beverages, the greater the perceived risk to insurers, leading to a higher restaurant insurance cost. This coverage protects you if a patron becomes intoxicated and causes harm to themselves or others. ### Claims History Your restaurant’s past claims history is a powerful predictor of future risk for insurers. If you have a history of frequent or costly claims, your restaurant insurance cost will likely be higher. Conversely, a clean claims record can help you negotiate lower premiums. Insurers view a history of claims as an indication of potential ongoing risks. ### Safety and Security Measures Proactive measures to enhance safety and security can positively impact your restaurant insurance cost. This includes: Fire Suppression Systems: Well-maintained sprinkler systems and fire extinguishers. Security Cameras: Visible surveillance systems can deter theft and aid in investigations. Regular Maintenance: Keeping premises in good repair to prevent slip-and-fall hazards. Employee Training: Comprehensive training on food safety, alcohol service, and emergency procedures. Demonstrating a commitment to safety can lead to discounts on your restaurant insurance cost. ## Components of Restaurant Insurance and Their Cost Implications A robust restaurant insurance policy is typically comprised of several distinct coverages, each contributing to the overall restaurant insurance cost. Understanding what each component covers is crucial for tailoring your policy to your specific needs. ### General Liability Insurance This is a foundational coverage for any restaurant. It protects your business against claims of bodily injury or property damage that occur on your premises or as a result of your operations. For example, if a customer slips on a wet floor and breaks their arm, general liability would cover their medical expenses and any legal fees if they sue. The restaurant insurance cost for general liability is influenced by your location, revenue, and the perceived risk of customer accidents. ### Liquor Liability Insurance As mentioned, if you serve alcohol, this coverage is non-negotiable. It protects your business from claims arising from serving alcohol to intoxicated individuals who then cause harm. The restaurant insurance cost for liquor liability can be substantial, especially for establishments with high alcohol sales. ### Property Insurance This coverage protects your physical assets, including the building (if you own it), equipment, furniture, and inventory, against damage from events like fire, theft, vandalism, or natural disasters. The restaurant insurance cost for property insurance depends on the value of your assets, the location of your restaurant, and the security measures in place. ### Business Interruption Insurance Also known as business income insurance, this coverage helps replace lost income and cover ongoing operating expenses if your restaurant is forced to close temporarily due to a covered event, such as a fire or a major flood. The restaurant insurance cost for business interruption is often bundled with property insurance, and its premium is influenced by your revenue and the potential duration of a shutdown. ### Workers’ Compensation Insurance This is legally mandated in most jurisdictions and covers medical expenses and lost wages for employees who are injured or become ill on the job. The restaurant insurance cost for workers’ compensation is heavily dependent on the number of employees, their job roles (e.g., a chef might have a higher risk than a host), and your state’s regulations. ### Food Spoilage Insurance This specialized coverage protects your restaurant against the loss of perishable food inventory due to power outages or equipment breakdown. If your refrigerators fail, leading to significant spoilage, this insurance can reimburse you for the lost product. The restaurant insurance cost for food spoilage is typically a smaller component of the overall policy but can be vital for businesses with a large inventory of fresh ingredients. ### Employment Practices Liability Insurance (EPLI) EPLI protects your restaurant against claims made by employees alleging discrimination, wrongful termination, harassment, or other employment-related issues. As your business grows and you employ more staff, the restaurant insurance cost associated with EPLI becomes increasingly relevant. ### Cyber Liability Insurance In today’s digital age, restaurants often handle sensitive customer data (credit card information, personal details). Cyber liability insurance protects your business in the event of a data breach, covering costs associated with notification, credit monitoring, legal fees, and regulatory fines. The restaurant insurance cost for cyber liability is influenced by the volume of data you handle and your data security practices. ## Estimating Your Restaurant Insurance Cost While it’s impossible to provide an exact figure without a personalized quote, understanding the factors and components allows for a more educated estimation of your restaurant insurance cost. Average Restaurant Insurance Cost Ranges (Illustrative – actual costs will vary significantly):Small Cafe/Deli: $500 – $2,000 per year Mid-size Casual Dining Restaurant: $1,500 – $5,000 per year Large Fine Dining Restaurant/Bar: $5,000 – $15,000+ per year These are rough estimates and should not be taken as definitive. The actual restaurant insurance cost will depend on the specific risk profile of your establishment. ### How to Get an Accurate Restaurant Insurance Cost Quote To obtain an accurate restaurant insurance cost, you will need to: 1. Gather Detailed Information: Be prepared to provide comprehensive details about your restaurant, including its location, type of cuisine, annual revenue, number of employees, operating hours, alcohol sales volume, and any past claims. 2. Contact Multiple Insurers or Brokers: It is highly recommended to get quotes from several different insurance providers or work with an independent insurance broker who specializes in restaurant insurance. This allows you to compare coverage options and pricing to find the best restaurant insurance cost for your business. 3. Be Honest and Thorough: Provide accurate and complete information. Misrepresenting facts can lead to denied claims and higher premiums in the future, impacting your long-term restaurant insurance cost. 4. Discuss Your Specific Needs: Clearly articulate the unique risks and operational aspects of your restaurant to ensure you are quoted for the most relevant coverages. By meticulously understanding the multifaceted nature of restaurant insurance cost, restaurateurs can approach the process with confidence, securing the protection their business needs while managing their financial obligations effectively.