Business Interruption Insurance Coverage – Imagine the unthinkable: a fire engulfs your storefront, a flood inundates your office, or a cyberattack cripples your operations. In the blink of an eye, your business grinds to a halt. This isn’t just a temporary inconvenience; it’s a potential financial catastrophe. This is precisely where Business Interruption Insurance Coverage steps in, acting as a crucial safety net for businesses navigating the unpredictable landscape of modern commerce. It’s designed to help you recover not just from the physical damage, but from the loss of income and ongoing expenses that arise when your business can’t operate as usual.

At its core, business interruption insurance is a form of coverage that reimburses a business for lost income and operating expenses if it’s forced to temporarily close due to a covered peril. This often includes events like natural disasters, fires, or even certain types of civil unrest, depending on the specific policy. It’s more than just covering the cost of repairs; it’s about bridging the financial gap while you get back on your feet. This means your rent, payroll, loan payments, and other essential operating costs can continue to be met, preventing a temporary setback from becoming a permanent closure. Without this vital protection, many businesses would struggle to survive even a short period of forced inactivity.

Understanding the nuances of business interruption insurance is paramount for any business owner. It’s not a one-size-fits-all solution, and the specifics of what’s covered, the duration of coverage, and the payout limits can vary significantly between policies and providers. Factors like the type of business, its location, and its susceptibility to various risks all play a role in determining the most suitable coverage. Furthermore, you should also consider the Business Liability Insurance Cost to ensure comprehensive protection for your firm. Proactively assessing your business’s vulnerabilities and consulting with an insurance professional can ensure you have the right level of protection in place, offering peace of mind and a clear path to recovery when the unexpected inevitably occurs.

Business Interruption Insurance Coverage

Navigating the complexities of business interruption insurance coverage is paramount for any enterprise seeking to safeguard its financial stability against unforeseen events. This type of insurance, often referred to as Business Income Insurance, is designed to compensate a business for lost income and cover ongoing operating expenses when operations are temporarily halted due to a covered peril. Understanding the nuances of business interruption insurance coverage, its triggers, limitations, and the process of making a claim is critical for proactive risk management.

Understanding the Core Purpose of Business Interruption Insurance Coverage

At its heart, business interruption insurance coverage acts as a vital safety net. It’s not about covering the physical damage to property itself, which is typically handled by a separate commercial property insurance policy. Instead, it focuses on the economic fallout resulting from that damage. Imagine a fire that forces your retail store to close for several weeks. While your property insurance might cover the cost of rebuilding, business interruption insurance coverage steps in to replace the profits you would have earned during that closure and helps pay for essential expenses like rent, payroll, and utilities that continue to accrue even when the doors are shut.

Key Triggers for Business Interruption Insurance Coverage

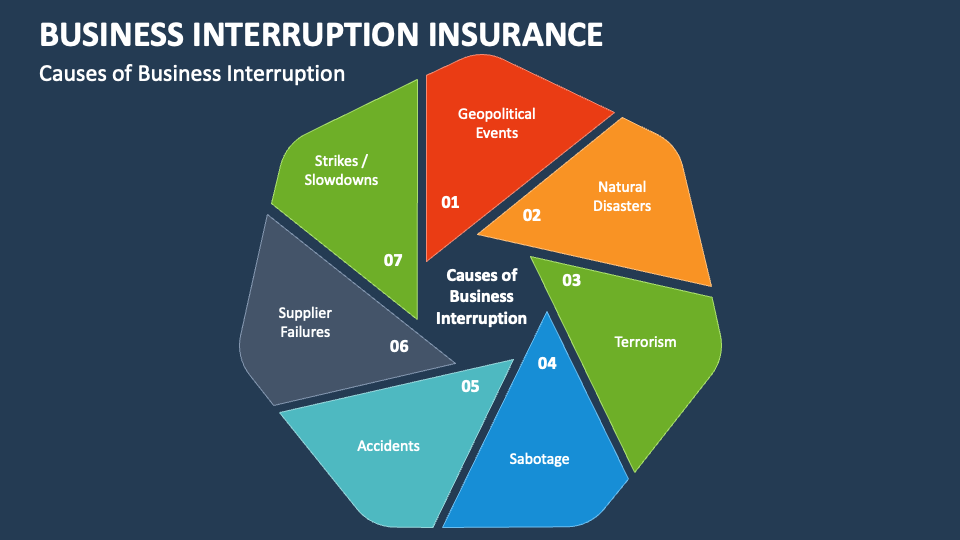

The activation of business interruption insurance coverage is contingent upon specific events, or perils, being explicitly listed and covered within the policy. While the exact list of covered perils can vary significantly between insurers and policy types, some of the most common triggers include:

- Fire: A widespread and common cause of business interruption.

- Windstorms and Hail: Damage to the physical structure that necessitates a shutdown.

- Vandalism and Malicious Mischief: Intentional damage leading to operational disruption.

- Lightning: Can cause significant damage to electrical systems and the building itself.

- Explosions: Similar to fire, an explosion can render a business premises unusable.

- Civil Authority: In some cases, if government authorities order a business to close due to a covered event affecting the vicinity (e.g., a gas leak or a public health crisis, though the latter is often a specific rider), business interruption insurance coverage may apply.

- Damage to Dependent Properties: Some policies extend coverage if a key supplier or customer experiences a covered loss that directly impacts your business’s ability to operate. This is often referred to as Contingent Business Interruption (CBI).

It is crucial to scrutinize your policy documents to understand precisely which perils are covered. Exclusions are just as important as inclusions; for instance, many standard policies do not cover interruptions due to pandemics, earthquakes, or floods unless specific endorsements are purchased.

Coverage Components within Business Interruption Insurance Coverage

A comprehensive business interruption insurance coverage policy typically includes several key components designed to address the multifaceted financial impacts of a shutdown:

- Lost Business Income: This is the primary benefit, aiming to replace the net income your business would have earned had the interruption not occurred. It usually includes profits and expenses that would have been earned.

- Continuing Operating Expenses: This covers ongoing costs that your business must continue to pay, regardless of whether it’s operational. Common examples include:

- Rent or mortgage payments

- Payroll for essential staff

- Utilities (electricity, water, gas)

- Loan payments

- Taxes

- Insurance premiums

- Extra Expense Coverage: This is a critical, often overlooked, component. Extra Expense coverage reimburses businesses for costs incurred to minimize the shutdown period or to keep the business operating at a reduced capacity at a temporary location. Examples include:

- Renting temporary office or production space

- Leasing replacement equipment

- Overtime wages for employees to expedite repairs or operations

- Costs associated with temporary advertising to inform customers of a new location

- Civil Authority Coverage: As mentioned, this can be a valuable rider, providing coverage when government action prevents access to your business premises due to damage to adjacent property caused by a covered peril.

- Contingent Business Interruption (CBI): This coverage protects against losses resulting from damage to a key supplier or customer’s business. If your primary supplier’s factory burns down, and you can’t get the raw materials you need, CBI can help offset your lost income.

- In-Transit or Off-Premises Property Coverage: Some policies may extend business interruption coverage to situations where property is damaged while being transported to or from your business or is located at an off-premises storage facility.

Determining the Right Amount of Business Interruption Insurance Coverage

One of the most challenging aspects of securing business interruption insurance coverage is determining the appropriate level of coverage. Underinsuring can leave a business exposed to significant financial hardship, while overinsuring can lead to unnecessary premium costs. The process typically involves a thorough analysis of your business’s financial data and operational needs:

- Calculate Annual Net Income: Review your historical profit and loss statements to determine your typical net income over a 12-month period.

- Identify Continuing Expenses: List all the expenses that will continue to accrue even if your business is shut down.

- Estimate Potential Shutdown Duration: Work with your insurance broker and consider the potential time it might take to repair or replace damaged property and resume operations after a significant event. This is often an educated guess, but it’s vital for determining the indemnity period.

- Assess Extra Expense Needs: Evaluate the potential costs associated with operating from a temporary location or expediting repairs.

- Consider Peak Season Impact: Ensure your coverage accounts for your business’s busiest periods. A shutdown during your peak season can be far more devastating than during a slow period.

Many policies have a set “indemnity period,” which is the maximum duration for which the business interruption insurance coverage will pay benefits. Common indemnity periods range from 6 to 12 months, but longer periods can be purchased for an additional premium. It’s crucial to select an indemnity period that realistically reflects the time needed to recover from a significant disruption.

The Claims Process for Business Interruption Insurance Coverage

Filing a successful claim for business interruption insurance coverage requires prompt action and meticulous documentation. The process generally involves the following steps:

- Notify Your Insurer Immediately: As soon as a covered event occurs and operations are interrupted, contact your insurance company or broker. Adhering to reporting deadlines is critical.

- Mitigate Your Losses: You have a duty to take reasonable steps to minimize the extent of your losses. This might involve relocating to a temporary site, using alternative suppliers, or incurring extra expenses to resume operations quickly. Keep detailed records of all mitigation efforts and associated costs.

- Gather Documentation: This is perhaps the most crucial step. You will need to provide extensive financial records to substantiate your claim. This includes:

- Profit and Loss Statements (monthly and annual)

- Balance Sheets

- Tax Returns

- Sales Records

- Payroll Records

- Bank Statements

- Lease Agreements

- Utility Bills

- Records of all continuing expenses

- Invoices for extra expenses incurred

- Work with the Adjuster: The insurance company will assign a claims adjuster to assess the damage and review your claim. Be prepared to provide them with all requested documentation and answer their questions thoroughly.

- Negotiate the Settlement: Based on the gathered evidence and the policy terms, the adjuster will propose a settlement. You may need to negotiate if you believe the offer does not adequately reflect your losses.

The claims process can be lengthy and complex. Having a good working relationship with your insurance broker and understanding your policy thoroughly beforehand can significantly ease this process.

Common Pitfalls and Considerations for Business Interruption Insurance Coverage

Several common pitfalls can hinder a business’s ability to benefit from its business interruption insurance coverage. Being aware of these can help you avoid them:

- Inadequate Policy Limits: Not purchasing enough coverage to match potential losses.

- Insufficient Indemnity Period: Choosing a period that is too short to realistically recover.

- Exclusions for Specific Perils: Overlooking critical exclusions such as pandemics, cyber-attacks, or natural disasters not covered by the base policy.

- Failure to Document Properly: Lack of detailed financial records or records of mitigation efforts.

- Delay in Reporting the Claim: Missing notification deadlines can jeopardize your claim.

- Not Understanding “Actual Loss Sustained”: Policies often pay for the “actual loss sustained” during the period of interruption, which requires careful calculation.

- Ignoring Extra Expense Coverage: Failing to adequately insure for the costs of resuming operations quickly.

- Cyber-Related Interruptions: Standard business interruption policies often do not cover losses stemming from cyber-attacks. Separate cyber insurance is typically required for this.

- Supply Chain Vulnerabilities: Not considering contingent business interruption coverage if your business heavily relies on a few key suppliers.

It is highly recommended to work with an experienced insurance broker who specializes in commercial insurance. They can help you assess your risks, understand your policy options, and ensure you have appropriate business interruption insurance coverage tailored to your specific industry and operational needs.

The Importance of Regular Review of Business Interruption Insurance Coverage

Your business is not static, and neither should your insurance coverage be. Regular reviews of your business interruption insurance coverage are essential. As your business grows, expands, or changes its operational model, your insurance needs will likely evolve. Factors such as increased revenue, changes in inventory, new locations, or reliance on new technologies can all impact the potential financial loss from an interruption. Schedule annual reviews with your insurance broker to ensure your policy limits, indemnity period, and covered perils remain aligned with your current business reality.